The efficient market hypothesis claims that share prices reflect risk to reward based on all available information. It is ultimately investors, and not companies, that determine valuation. Companies are largely powerless to improve low valuations unless they buyback shares which boosts EPS and can temporarily drive shares higher through share demand. But when perceived risk reaches so high that valuations become ridiculously low, companies have another tool at their disposal to support slumping share prices. Whether they do so or not is another matter.

What could Chinese small-cap companies do to bring investors back to the table and lower risk?

Chinese Small-Cap Scandal

Last year we saw a lot of frustrated investors as Chinese small caps were pounded down hard. American investors dumped these publicly traded reverse mergers regardless of the seeming deep value. Investors disregarded price-to-earnings and cash holdings as the risk of de-listing or bankruptcy due to fraud loomed. Even if these Chinese small-caps stayed listed, what guarantee do investors have that they will have improving valuations over time? Maybe a P/E of 2 or 3 is the new normal for these higher risk firms.

The Beauty of Dividends

One tool a company has at its disposal when valuations become too low is dividends. If enough the P/E ratio is low enough to provide very high yields for shareholders, the risk of loss drops dramatically each year. Consider one such example:

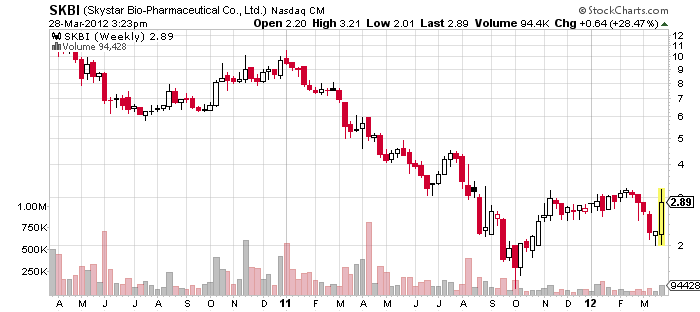

Skystar Bio-Pharmaceutical (SKBI) is a Chinese veterinary health care company. Share price sits at $2.81 with recent risk of Nadaq de-listing (share prices are volatile, as they were just granted continued listing). There is no guarantee that holding this stock will result in any return over time and you might simply hold it until it is de-listed one day in the future as prices fall further. How might the decision to pay dividends affect the share price going forward?

The company holds 59 cents cash per share. The company is on target for making $2.25 per share in the 2011 fiscal year and the same amount next year. What if the company decided to throttle back on capital expenditures somewhat to pay a dividend in an effort to boost share value? If it paid out 70% of earnings and assuming that this new policy would lower earnings forecasts to two dollars per share, similar to last year, investors would receive a 50% dividend yield. Even if share prices jumped to $4.20 you would still receive a 33% yield. After gaining back shareholder confidence by putting large sums of cash in their pockets, these Chinese small-caps could consider reducing or eliminating dividends to focus on future growth. Of course, they could keep this policy in effect as long as necessary to quell fear.

Other Dividend Potentials

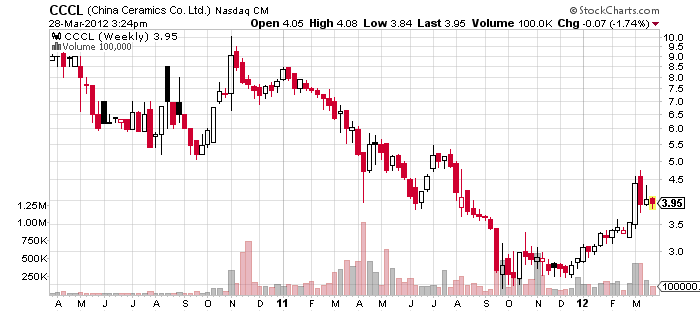

China Ceramics (CCCL) is another company that could help its share price by introducing a dividend. It trades at $3.88 per share and has an earning expectation of $2.69 per share in 2012. That represents a theoretical upper limit of a 69% yield if share prices remained static. Even a "small" dividend announcement with a 30% payout ratio would deliver a whopping 21% yield. Either share prices would be supported at much higher levels or current investors would feel more secure as they put real cash in their bank accounts while the high-risk Chinese small-cap scenario played out.

SORL Auto Parts (SORL) trades at a trailing and forward P/E ratio of 3.3. Earnings are expected to be $0.90 for the 2011 FY and $1.00 for 2012. They have 64 cents in cash and the price is at $3.35 per share. With book value at almost $8 per share, it is clear that any equity held by the company is being steeply discounted. They could easily take one-third of their earnings to pay shareholders a 10% dividend.

Other Chinese small-caps with incredibly low P/E ratios are Dehaier Medical Systems Limited (DHRM), with a P/E of 2.27, and Sutor Technology Group Limited (SUTR), with a trailing P/E of 2.81 and a forward P/E of 2.1. Consider what Deer Consumer Products (DEER) has achieved with a lowly 14% payout ratio - a forward 5.8% yield. While this is a good start I think that these smaller firms should increase payout for big yields that will improve their public image while lowering investor risk. This isn't the Greece bond scenario as these companies do have the cash and earnings to pay the yield.