The efficient market hypothesis claims that share prices reflect risk to reward based on all available information. It is ultimately investors, and not companies, that determine valuation. Companies are largely powerless to improve low valuations unless they buyback shares which boosts EPS and can temporarily drive shares higher through share demand. But when perceived risk reaches so high that valuations become ridiculously low, companies have another tool at their disposal to support slumping share prices. Whether they do so or not is another matter.

What could Chinese small-cap companies do to bring investors back to the table and lower risk?

Chinese Small-Cap Scandal

Last year we saw a lot of frustrated investors as Chinese small caps were pounded down hard. American investors dumped these publicly traded reverse mergers regardless of the seeming deep value. Investors disregarded price-to-earnings and cash holdings as the risk of de-listing or bankruptcy due to fraud loomed. Even if these Chinese small-caps stayed listed, what guarantee do investors have that they will have improving valuations over time? Maybe a P/E of 2 or 3 is the new normal for these higher risk firms.

The Beauty of Dividends

One tool a company has at its disposal when valuations become too low is dividends. If enough the P/E ratio is low enough to provide very high yields for shareholders, the risk of loss drops dramatically each year. Consider one such example:

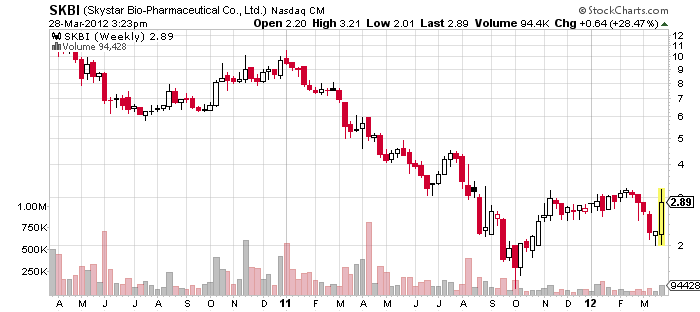

Skystar Bio-Pharmaceutical (SKBI) is a Chinese veterinary health care company. Share price sits at $2.81 with recent risk of Nadaq de-listing (share prices are volatile, as they were just granted continued listing). There is no guarantee that holding this stock will result in any return over time and you might simply hold it until it is de-listed one day in the future as prices fall further. How might the decision to pay dividends affect the share price going forward?

The company holds 59 cents cash per share. The company is on target for making $2.25 per share in the 2011 fiscal year and the same amount next year. What if the company decided to throttle back on capital expenditures somewhat to pay a dividend in an effort to boost share value? If it paid out 70% of earnings and assuming that this new policy would lower earnings forecasts to two dollars per share, similar to last year, investors would receive a 50% dividend yield. Even if share prices jumped to $4.20 you would still receive a 33% yield. After gaining back shareholder confidence by putting large sums of cash in their pockets, these Chinese small-caps could consider reducing or eliminating dividends to focus on future growth. Of course, they could keep this policy in effect as long as necessary to quell fear.

Other Dividend Potentials

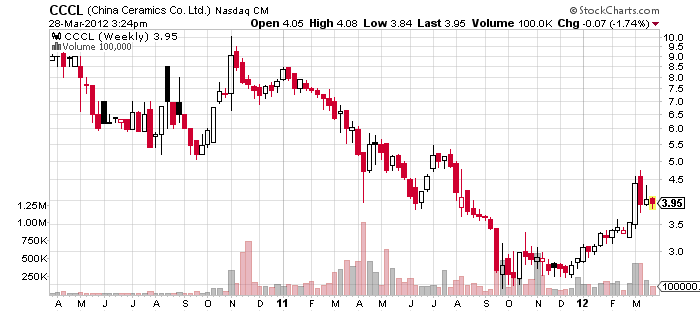

China Ceramics (CCCL) is another company that could help its share price by introducing a dividend. It trades at $3.88 per share and has an earning expectation of $2.69 per share in 2012. That represents a theoretical upper limit of a 69% yield if share prices remained static. Even a "small" dividend announcement with a 30% payout ratio would deliver a whopping 21% yield. Either share prices would be supported at much higher levels or current investors would feel more secure as they put real cash in their bank accounts while the high-risk Chinese small-cap scenario played out.

SORL Auto Parts (SORL) trades at a trailing and forward P/E ratio of 3.3. Earnings are expected to be $0.90 for the 2011 FY and $1.00 for 2012. They have 64 cents in cash and the price is at $3.35 per share. With book value at almost $8 per share, it is clear that any equity held by the company is being steeply discounted. They could easily take one-third of their earnings to pay shareholders a 10% dividend.

Other Chinese small-caps with incredibly low P/E ratios are Dehaier Medical Systems Limited (DHRM), with a P/E of 2.27, and Sutor Technology Group Limited (SUTR), with a trailing P/E of 2.81 and a forward P/E of 2.1. Consider what Deer Consumer Products (DEER) has achieved with a lowly 14% payout ratio - a forward 5.8% yield. While this is a good start I think that these smaller firms should increase payout for big yields that will improve their public image while lowering investor risk. This isn't the Greece bond scenario as these companies do have the cash and earnings to pay the yield.

BELEGGEN IN EXTREEM IN ELKAAR GETRAPTE CHINESE AANDELEN

BeantwoordenVerwijderenKoers/Winst Verhoudingen Van Gemiddeld Onder De 3...!

25 aandelen die terecht of onterecht op een extreem lage waardering terecht zijn gekomen. Sir Tempelton werd ooit rijk door een portefeuille vol met 1 dollar aandelen te kopen. We hebben nu de TempleTom collectie van 25 spotgoedkope Chinese aandelen!

Beleggen kan je zo moeilijk maken als je zelf wilt. Uiteindelijk blijkt achteraf toch steeds weer dat je goedkoop moet kopen en duur moet verkopen. Dat is de beste strategie.

Wat beleggers maar niet begrijpen, is dat aandelen die 'goedkoop' zijn, ook impopulair zijn. Immers zouden ze anders niet meer goedkoop zijn. Om dus succes te hebben, moet je kopen wat anderen op dat moment niet willen hebben en je moet verkopen wat iedereen op dat moment aan het kopen is. De meeste beleggers doen het anders om.

Ik hoop dat u begrijpt wat hierboven staat.

Tegendraads beleggen wordt vaak gezien als kopen als de koersen dalen. Dat is echter onzin. U moet kopen als anderen een waarde die bedrijven bezitten niet naar de volle waarde inschatten. Dat heeft dus niets te maken met dalende koersen. U moet puur kijken naar wat of een bedrijf waard is en welke kansen het biedt. Wat de koers nu of morgen doet, is irrelevant.

Pak kansen die anderen, om welke reden dan ook, niet zien.

Om die reden ben ik gaan zoeken in China. Mogelijk hoorde u al van de fraude van Chinese bedrijven die in Amerika op de beurs een Reverse Take over deden om via die weg in Amerika op de beurs te komen. Naar is gebleken waren er een aantal bedrijven die vervolgens twee boekhoudingen aanhielden. Een Chinese boekhouding en een Amerikaanse. In Amerika werden de cijfers veel mooier gepresenteerd. Dit om veel Amerikaanse beleggingsgeld te verkrijgen. Helaas lijken enkele fraudes wel degelijk bewezen te gaan worden en was er in enkele gevallen sprake van grove boze opzet.

Vanuit dat gegeven is vervolgens ieder Chinees aandeel verdacht geworden en zien we dat beleggers deze aandelen massaal de rug toekeerden. Dalingen van meer dan 90% zijn geen uitzondering gebleken. Vervelend voor de zittende aandeelhouders, maar wat een kans voor beleggers die goedkoop willen kopen! Niet omdat de koersen gedaald zijn, want dat boeit me niet zo. Wat veel belangrijke is, is dat de fundamentele cijfers nu zo mooi zijn. Koers/Winst verhoudingen van 1 tot 7, PEG ratio's van onder de 0,2 tot 1, Dat alles soms ook nog met een positieve cash flow. Allemaal zaken die voor een tegendraadse belegger heel interessant zijn.

2)

BeantwoordenVerwijderenWaarom laten beleggers dit soort buitenkansjes liggen?

Nu, dat is simpel. De kans bestaat dat er nog altijd enkele bedrijven zijn die nog niet gesnapt zijn... Dat is dan ook de reden dat ik 25 van die extreem goedkope Chinese aandelen bij elkaar heb gezocht. 25 keer hetzelfde bedrag in deze aandelen. Misschien blijken er enkele toch fraudes te zijn, maar de kans dat ze alle 25 een fraude zijn, is vrijwel uitgesloten. Sterker nog, ik heb de verwachting dat het met die fraudes uiteindelijk wel mee zal vallen. China is nu eenmaal een economie in opkomst. Heel bewust heb ik dan ook gekeken hoe veel schorters er in een aandeel zaten.

Uit een selectie van uiteindelijk zo'n 50 aandelen heb ik er 25 uitgekozen die in mijn portefeuille terecht mogen komen. Ik ga vervolgens 25 keer een zelfde bedrag in deze aandelen stoppen. Bij de één houdt het in, 500 aandelen, bij de ander misschien 25 aandelen. De koers van het aandeel is geen indicatie voor de waardering. In het rapport vindt u de naam en de code van alle aandelen. U vindt de K/W, de PEG, de Cash Flow indicatie.

Wat de bedrijven verder doen, is voor mij niet interessant. We kopen puur 25 stukken omdat ze extreem laag gewaardeerd zijn.

Let op! Als u niet de intentie heeft om alle 25 aandelen te kopen, dan moet u dit rapport niet bestellen! Als u verwacht dat ik meer dan het bovenstaande ga uiteenzetten over de bedrijven achter de aandelen, moet u dit rapport niet bestellen. Als u zekerheid wilt en geen risico wilt lopen, moet u dit rapport niet bestellen.

Wilt u echter laag kopen, dan is dit uw kans. De waarderingen zijn echt extreem te noemen. In Nederland en België vindt u echt geen aandelen met een K/W van 3.

Bestelt u daarom nu dit Nederlandstalige TempleTom Chinese aandelenrapport en profiteer van ongekende onderwaarderingen. Het kost u eenmalig 48 euro. Zodra uw overboeking binnen is, sturen we u het rapport per E-mail toe!

Nota Bene: In dit rapport treft u een flink aantal zeer interessante en opmerkelijke Chinese aandelen met beursnotering in Amerika aan. Aandelen die niet op de beurs van Amsterdam en Brussel genoteerd staan, maar wel op de Amerikaanse beurzen. U moet zelf even bij uw broker of bank nagaan of u kunt beleggen in aandelen die in Amerika of Canada genoteerd staan. (Zover ons bekend kunt u met TradersOnly, Lynx, Alex, Binck, Interactive Brokers en ABNAMRO uiteindelijk wel beleggen in de meeste van deze aandelen)

http://www.beursaccent.nl/templetom/index.php

Precies Mar 28, 2012 07:24 AM

BeantwoordenVerwijderen-------------

Is Xinyuan Real Estate The World's Cheapest Stock?

March 28, 2012 | 13 comments | about: XIN, includes: KBH, TOL

By: Jared Sleeper

Xinyuan Real Estate (XIN) may well qualify as the world's cheapest stock. Xinyuan is a real estate developer in China that builds massive housing developments in China's tier 2 and 3 cities (not Beijing, Shanghai or Guangzhou, which are considered tier 1), selling units to China's burgeoning middle class. The company was founded in 1997, and launched an initial public offering on the New York Stock Exchange in December of 2007, becoming the first Chinese real estate company to do so.

Xinyuan originally appeared on our radar because the stock appears cheap. Very, very cheap. The company's market capitalization of roughly $200 million is backed up by $100 million in net income last year (and $100 million projected for next year as well), $487 million in cash and cash equivalents and $768 million in tangible assets (in this case, primarily housing inventories). This is offset by $285 million of outstanding debt (short- and long-term), and additional considerations such as accounts payable totaling (all together) roughly $500 million. The undervalued nature of Xinyuan's stock doesn't take complicated ratios to see, it is a matter of arithmetic. The $487 (cash in millions) + $786 (assets in millions) - $750 million (total liabilities) = $523 million, more than two and a half times the company's current market cap. In terms of valuing the company's income, a conservative valuation of 5X earnings (trailing or forward projected) yields a valuation of $500 million, again roughly 250% higher than current valuations.

With this in mind, we set out to determine why a real estate developer in one of the fastest growing regions on earth might be selling at a forward P/E of 2 with a substantial cash position. We found two primary reasons that we believe explain the disparity. The first is that the market perceives a risk of fraud. This has been a huge concern for all Chinese small cap companies traded in the U.S. Many investors, both large and small, have been burned by Chinese companies that were completely fraudulent, often companies listed on U.S. exchanges through the reverse merger process. As we will explain below, we feel very confident that Xinyuan is not a fraud.

etc,etc.

http://seekingalpha.com/article/462341-is-xinyuan-real-estate-the-world-s-cheapest-stock

----------------

NB: verplaatst van China algemeen

The Perfect Time To Invest In Perfect World

BeantwoordenVerwijderenMay 30, 2012 | 4 comments | about: PWRD, includes: ATVI, HAS, NTES

Shares of gaming company Perfect World (PWRD) dropped over 13% in after hours trading on Tuesday night. Shares closed at $10 a share after the late trading session had ended. Perfect World shares continue to fall during Wednesday's trading session and now are below $10. I think the downfall is overblown and now represents a good time to take a long term bet on the Chinese gaming company.

During the first quarter, Perfect World had no major launches of games. The company did release several expansion packs and utilized its international expansion.

Launched Star Trek MMORPG in Germany and France

Released an expansion pack for Dragon Excalibur

Released an expansion pack for Hot Dance Party

Released Blacklight Retribution, a free to play shooting game, in North America and Europe

Licensed Battle of Immortals in the Brazilian market

Released Forsaken World and Chi Bi in Indonesia

Launched Forsaken World into Brazil

Financials of the company's first quarter are likely what scared investors away from Perfect World's shares. Revenue for the first quarter was flat, on a year-over-year basis. The revenue was down from the company's recent fourth quarter. Licensing revenue, which had been a recent strong point, was also down during the company's first quarter. The financials were hurt due to no new releases. The company also touched briefly on the Chinese New Year and how the celebration kept people away from computers and led to lower in-game monetization. The company's operating profit and net income both saw declines as well. Diluted earnings per share came in at RMB4.52, compared to RMB5.45 during last year's first quarter.

Guidance for the second quarter calls for revenue of RMB647-RMB683 million. This is a decline from fiscal 2011's second quarter revenue totals.

Perfect World's pipeline of games remains strong and is ever expanding:

Another new game from Perfect World is Fantasy Condor Heroes. The MMORPG is based on a Chinese novel titled Return of the Condor Heroes, written by Louis Cha. The game will be released in the summer of 2012.

Heaven Sword and Dragon Saber will be releasing in the first half of 2013.

Saint Seiya Online, based on a Japanese title of the same name also written by Louis Cha, will be released in the first quarter of 2013.

Forsaken World will be released through the company's partnership with Nexon in South Korea.

Perfect World also has two games being designed by its studios in the United States. Torchlight and Neverwinter are being designed in America and will then also be tested in the Chinese market before they are released. Both games are being developed as free to play games. Neverwinter is scheduled to be released in 2013.

Expansion pack for Zhu Xian during the company's second quarter.

Expansion pack for Perfect World II in quarter 3 or quarter 4 for the company.

Forsaken World expansion pack in second half of fiscal 2012.

Mentioned above, the company's U.S. studios are developing a game called Neverwinter. The game was recently announced as a showcase at the E3 (Electronic Entertainment Expo) June 5th through June 7th. The game is based on the successful Dungeons & Dragons franchise. People who attend the booth can play a demo of the upcoming Perfect World release. The game was announced back in 2010 but has been delayed because of Perfect World's acquisition of the studio from Atari, and a switch to a free to play game format. The game could be a huge launch with an already built in brand of Dungeons & Dragons. Wizards of the Coast, a subsidiary of Hasbro (HAS) was also working on new product releases to coincide with the game's launch.

During the question and answer segment of the conference call, Perfect World management was asked about a possible expansion into social games. The company responded that they already have released two SNS games in China and have a current team working on possible expansion.

BeantwoordenVerwijderenThe fourth quarter earnings for Perfect World were record breaking and saw the company declare a special $2 a share dividend. Revenue in the quarter grew over 25% from the previous year's fourth quarter. During the question and answer segment, the company confirmed that they are looking at paying out a dividend each year, depending on profits and cash levels. The dividend will be proposed by the chief executive officer and then voted on by the board of directors. Perfect World also mentioned a possible share buyback as the best use of its existing cash balance.

During the fourth quarter, Perfect World also announced a partnership with Nexon, the large gaming company from South Korea. The partnership will allow Perfect World to grow in South Korea. The move is part of a continuing international expansion of the company. Perfect World now licenses its games in over 100 countries. International business makes up 25% of Perfect World's revenue.

Competition for Perfect World remains intense with gaming companies based in China and in other countries as well. Netease (NTES) is one of the company's biggest rivals and offers World of Warcraft to the Chinese market, through a partnership with Activision Blizzard (ATVI). Perfect World has grown through ramping up the number of releases each year. The company has also focused on releasing expansion packs to further the life cycle of many of its hit games.

Perfect World has a great portfolio of games releasing in late 2012 or early 2013. The shares could trade down for awhile with no new blockbuster games until late 2012. The company has some clear strategies in place in expansion packs and international licensing. I like the concept of the Neverwinter game and think it could be a big launch for the company. I would recommend buying shares of the company at anything under $11. I think shares could trade back in the $20 range next year at this time.

Disclosure: I am long ATVI.

by Chris Katje »

http://seekingalpha.com/article/626421-the-perfect-time-to-invest-in-perfect-world?source=yahoo

Income Statement

VerwijderenRevenue (ttm): 470.11M

Revenue Per Share (ttm): 9.64

Qtrly Revenue Growth (yoy): 32.30%

Gross Profit (ttm): 397.76M

EBITDA (ttm)6: 188.03M

Net Income Avl to Common (ttm): 155.05M

Diluted EPS (ttm): 3.03

Qtrly Earnings Growth (yoy): 107.70%

Balance Sheet

Total Cash (mrq): 360.80M

Total Cash Per Share (mrq): 7.81

Total Debt (mrq): 88.36M

Total Debt/Equity (mrq): 14.07

Current Ratio (mrq): 1.89

Book Value Per Share (mrq): 13.51

Cash Flow Statement

Operating Cash Flow (ttm): 181.49M

Levered Free Cash Flow (ttm): 36.39M

Market cap 500 miljoen

koers/winstverhouding ca 3,5 voor 2012 en ca 2 op basis van de taxaties voor 2013.

http://finance.yahoo.com/q/ae?s=PWRD+Analyst+Estimates

Top Institutional Holders:

VerwijderenHolder Shares % Out Value* Reported

JP MORGAN CHASE & COMPANY 2,380,285 5.15 38,513,011 Mar 30, 2012

PUTNAM INVESTMENT MANAGEMENT, LLC 1,621,352 3.51 26,233,475 Mar 30, 2012

Susquehanna International Group, LLP 1,608,844 3.48 26,031,095 Mar 30, 2012

ACADIAN ASSET MANAGEMENT 1,525,744 3.30 24,686,537 Mar 30, 2012

Cavalry Management Group, LLC 1,347,703 2.92 21,805,834 Mar 30, 2012

Alpine Woods Capital Investors, LLC 1,234,900 2.67 19,980,682 Mar 30, 2012

RENAISSANCE TECHNOLOGIES, LLC 1,202,600 2.60 19,458,068 Mar 30, 2012

WELLINGTON MANAGEMENT COMPANY, LLP 1,095,154 2.37 11,466,262 Dec 30, 2011

FIL LTD 1,048,493 2.27 16,964,616 Mar 30, 2012

FMR LLC 741,200 1.60 11,992,616 Mar 30, 2012

Top Mutual Fund Holders:

Holder Shares % Out Value* Reported

EMERGING MARKETS GROWTH FUND 611,600 1.32 6,403,452 Dec 30, 2011

PUTNAM VOYAGER FUND 603,227 1.31 6,466,593 Jan 30, 2012

VARIABLE INSURANCE PRODUCTS FD-OVERSEAS PORTFOLIO 475,100 1.03 7,687,118 Mar 30, 2012

PUTNAM INTERNATIONAL EQUITY FUND 339,000 0.73 3,549,330 Dec 30, 2011

ADVISORS INNER CIRCLE FUND-ACADIAN EMERGING MARKETS PORT 299,451 0.65 3,210,114 Jan 30, 2012

FIDELITY PACIFIC BASIN FUND 216,775 0.47 3,507,419 Mar 30, 2012

FIDELITY ADVISOR OVERSEAS FUND 203,400 0.44 3,291,012 Mar 30, 2012

SUNAMERICA SERIES TRUST-EMERGING MARKETS PORTFOLIO 181,686 0.39 1,947,673 Jan 30, 2012

PUTNAM VARIABLE TRUST-INTERNATIONAL EQUITY FUND 129,000 0.28 1,350,630 Dec 30, 2011

RS Investment Trust-Technology Fund 115,540 0.25 1,869,437 Mar 30, 2012

Value shown is computed using the security's price on the report date given.

Currency in USD.

http://finance.yahoo.com/q/mh?s=PWRD+Major+Holders

Schroders ziet Chinese koopjes

BeantwoordenVerwijderen11 Jun 2012 om 16:00 - IEXProfs Redactie - Gerelateerde onderwerpen: China, wereldeconomie

De groeivertraging van de Chinese economie zal spoedig koopjes opleveren op de beurzen van het land. Dat voorspelt Laura Luo, manager Chinese aandelen bij Schroders Investment Management. De eurocrisis en de kwakkelende Amerikaanse economie treffen de exporterende bedrijven in China. Maar "consumentenondernemingen groeien nog altijd sterk, een indicatie dat de Chinezen hun geld niet in hun zak houden".

Het blijft echter wel uitkijken geblazen in een "eigenaardige", verre van vrije markt als China. Zoals met de Chinese banken en hun omvangrijke leningen aan lokale overheden. Technologiebedrijven blijven wel aantrekkelijk, net als de energiesector als gevolg van "veranderende patronen in de consumptie op het platteland". Industriële bedrijven lijden onder de eurocrisis en de stagnatie in de VS. Maar anders dan Europa kan China "uit zijn huidige problemen groeien".

De noodzakelijke omschakeling van de Chinese economie van export naar meer binnenlandse consumptie is een "delicaat karwei". Maar tot dusver heeft de Chinese overheid dit proces bekwaam weten te begeleiden zonder de financiële markten kippenvel te bezorgen. "De doelstelling van 7,5 % groei in 2012 behoort nog steeds tot de meest ambitieuze op aarde," aldus Luo. "Zelfs inclusief de vertraging blijft China veel harder groeien dan welk ander land ook."

Perfect World - A Perfect Buying Opportunity

BeantwoordenVerwijderenAugust 3, 2012 | about: PWRD

Perfect World (PWRD) is a Chinese online game company that develops and publishes Massively Multiplayer Online Role Playing Games (MMORPGs) both in mainland China and abroad. In fact, Perfect World is one of the only game developers based in China to license and publish many of their titles over seas. International revenue for Perfect World currently accounts for ~25% of total revenues.

Despite strong sales growth, international expansion, and consistent profitably, Perfect World has drifted from its 52 week high of $23 to under $10 as of this writing. The reason for the collapse in stock price from a high of $46.69 in November 2009 has more to do with anxiety surrounding Chinese companies than fundamentals. Many retail investors, and even world-renowned hedge fund managers (John Paulson for example) have been left holding the bag once Chinese firms like SINO-Forest, China MediaExpress, and RINO International have been exposed for the frauds that they are.

Even though Perfect World was never accused of being a fraud the company's stock seems to have sold off as investors have seemingly thrown out the baby with the bath water when shedding their exposure to smaller Chinese companies. So is Perfect World a fraud? I think not, but lets look at the facts.

Corporate Structure

Like all Chinese companies traded in the U.S., Perfect World has an odd corporate structure. Each share of Perfect World traded in the U.S. Represents 5 ordinary shares of Perfect World Co., LTD, which is based in the Cayman Islands. The Cayman Islands-based company is a holding company for the various Perfect World subsidiaries around the world.

Due to various regulations in China, foreigners cannot own licenses to operate online games. In order to "get around" this rule, Perfect World's wholly owned Chinese division PW Software doesn't directly operate any games or generate any actual business. Instead, all of Perfect World's game operating activities in China are done through a company called PW Network which isn't directly owned by Perfect World, but PW Software (The Chinese subsidiary of Perfect World) has various contracts with PW Networks which essentially allows PW Software to control every aspect of PW Network's business operations. Despite PW Networks not being directly owned by Perfect World, the company is still, for all intents and purposes, a subsidiary of Perfect World.

So if Perfect World doesn't directly own PW Network, who does? Mr. Michael Yufeng Chi - Perfect World's CEO. This may seem shady at first glance, but the shareholders of PW Network have pledged ALL of their equity interests in their company to PW Software, which severely limits their ability to control PW Network, until the equity pledge expires on March 9th, 2024. On top of the equity pledge, PW Software owns a call option for PW Network which allows PW Software to purchase all of PW Network for the higher of RMB 10,000 or the minimum amount permitted by applicable law. PW Software can exercise this call option at its sole discretion up until the call option agreement expires on March 9, 2024.

Lastly, to further cement PW Software's control over PW Network the company has Power of Attorney over PW Network's assets. Despite the complex corporate structure shareholders in Perfect World do have claims to the Chinese assets, as Perfect World's Chinese subsidiary has full control of PW Network. All of this is clearly explained in Perfect World's 20-F filing under the headline "Risks Related to our Corporate Structure".

2)

BeantwoordenVerwijderenFosun Investment

On July 7th, 2012 Fosun International Ltd revealed in an SEC 13D filing that it had acquired 8.31%, or 3,443,230 American Depository Shares, of Perfect World on the open market at an average price of ~$10.32 per share. This investment in Perfect World is a major boost in the company's credibility, as the largest privately owned conglomerate in Mainland China would not be purchasing shares of a company without first verifying its legitimacy.

This isn't the first time Fosun International has purchased shares in Chinese companies traded in the U.S. at opportunistic times. As per their SEC filings, Fosun purchased 13.33% of shares in Focus Media Holdings (FMCN) back in December, 2008 and further increased their stake through numerous purchases to 28.65% by March 24, 2009. The stock traded at around $5-$8 during this period. On September 24, 2010 Fosun sold down its stake in Focus Media to 21.05% by selling shares at $21.

Buying at $5-$8 and selling at $21 netted Fosun international a phenomenal return on their investment. Focus Media is trading at around $19 now. Fosun was purchasing shares in Focus Media at dirt cheap prices because the company's stock price had just plummeted after Muddy Waters accused the company of fraud.

I suspect that Fosun took a large stake in Focus Media because they did their own homework and determined that the company was in fact legitimate. I suspect Fosun did their homework with Perfect World as well.

Dividend / Solid Balance Sheet

Perfect World issued a cash dividend of $98 million ($2 per share) in April 2012. The fact that the company had $98 million to distribute to shareholders is further proof that the company does in fact have the cash it claims it does. The $2 dividend in April was the first dividend to ever be paid out by Perfect World, and the company hinted that it may continue to pay dividends annually going forward. Even after paying the $98 million dividend, the company still had $221.5 million in cash and cash equivalents as per their 6-K filing.

The company's entire market cap is less than $500 million (as of July 31, 2012) - which means that nearly half of the market cap is net cash. The company has some short-term bank loans outstanding, but these were offset by the company's restricted cash, which was not included in the $221.5 million figure quoted. Add in the $197 million in property, equipment and software - and we're at $418.5 million in value simply counting the company's cash and headquarters. The company's book value (assets - liabilities) as per the most recently quarterly report is $574.9 million (Q1 2012). Even if you discount the intangible assets and goodwill, the company is trading below its current market cap.

3)

BeantwoordenVerwijderenCEO Ownership

As per the SC-13G filing with the SEC on February 13, 2012 the CEO of Perfect World Michael Yufeng Chi owned 35% of the outstanding shares in perfect World. He owned 17.5% directly and another 17.5% through a holding company he controls. The CEO of Perfect World clearly has a vested interesting in seeing the company succeed, and would benefit from continued dividend payments.

Auditor with a Flawless Record

Perfect World's annual reports are signed off by PWC Zhong Tian - the same independent auditor responsible for auditing the financial for NetEase.com (NTES), SINA Corporation (SINA), Sohu.com Inc (SOHU), and many other large Chinese companies. As an auditor, PWC Zhong Tian has a flawless record. Fellow Seeking Alpha contributor Adam Gefvert has a great write up on PWC Zhong Tian which is worth reading.

Conclusion

With a P/E of less than 4, solid balance sheet, and growing international presence - I strongly believe that Perfect World is severely mispriced at current levels. The current stigma surrounding small to medium sized Chinese companies traded in the U.S. has created a buying opportunity for those willing to buy and hold until sentiment changes.

Disclosure: I am long PWRD.

Omer Altay

This article was sent to 369 people who get email alerts on PWRD.

Get email alerts on PWRD

Xinyuan Real Estate Co., Ltd. Announces Second Quarter 2012 Financial Results

BeantwoordenVerwijderen-- Completes Best Quarter in History with Record Revenue, Contract Sales and Net Income

-- Company Raises FY12 Financial Forecast

Press Release: Xinyuan Real Estate Co., Ltd. – 17 minutes ago

Symbol Price Change

XIN 2.59

BEIJING, Aug. 10, 2012 /PRNewswire-Asia/ -- Xinyuan Real Estate Co., Ltd. ("Xinyuan" or "the Company") (XIN), a residential real estate developer with a focus on high growth, strategic Tier II cities in China, today announced its unaudited financial results for the second quarter of 2012.

Highlights for the Second Quarter 2012

Total second quarter revenues were US$253.1 million, a 38.5% increase from US$182.7 million reported in the second quarter of 2011, and a 46.6% increase from US$172.6 million recorded in the first quarter of 2012.

Contract sales totaled US$258.0 million, a 14.5% increase from US$225.3 million recorded in the second quarter of 2011, and a 61.6% increase from US$159.7 million recorded in the first quarter of 2012.

Total gross floor area ("GFA") sales were 194,500 square meters, a 6.1% increase from 183,400 square meters sold in the second quarter of 2011 and a 69.7% increase from 114,600 square meters sold in the first quarter of 2012.

Selling, General, and Administrative ("SG&A") expenses as a percent of total revenue totaled 6.2% compared to 5.6% in the second quarter of 2011 and 6.9% in the first quarter of 2012.

Income taxes resulted in a net benefit of US$5.8 million in the second quarter as four projects were settled with the tax authority and the related accrued liabilities were reversed with a net benefit of US$26.6 million recognized in the second quarter.

Net income reached US$69.4 million, a 118.2% increase from US$31.8 million reported in the second quarter of 2011 and a 199.1% increase from US$23.2 million in the first quarter of 2012.

Diluted net earnings per American Depositary Share ("ADS") attributable to shareholders were US$0.94, compared to diluted net earnings per ADS of US$0.40, in the second quarter of 2011 and US$0.31 per ADS, in the first quarter of 2012.

Cash and cash equivalents, including restricted cash, increased by US$89.0 million to US$604.7 million as of June 30, 2012 from US$515.7 million as of March 31, 2012. Short and long term debt decreased by US$53.8 million to US$228.9 million compared to US$282.7 million as of March 31, 2012.

Yesterday, August 9, 2012, the Company acquired a parcel of land In Suzhou with a total GFA of approximately 128,000 square meters at a cost of RMB270 million(US$42.6 million).

Mr. Yong Zhang, Xinyuan's Chairman and Chief Executive Officer said, "We were pleased to report the best quarter in our operating history with record contract sales, revenue and net income. As China's central bank reduced the reserve requirement ratio and interest rates were lowered to stimulate the economy, the real estate market responded with strong demand. All of our major projects experienced healthy levels of GFA sales and ASP trends."

"Our balance sheet continued to strengthen as our cash increased by US$89 million, while our debt was reduced by US$54 million. Meanwhile, our quarterly dividend payment continued in the second quarter and in June we announced an additional US$20 million share buyback program after completing the US$10 million share buyback program initiated in May 2011."

"Based on the current market environment, we believe that 2012 will be a record year for Xinyuan and we are adjusting our full year financial forecast accordingly. We continue to seek attractive land acquisitions at reasonable prices to ensure the future development and growth of our business. Our focus on affordable developments targeting homeowners in Tier II and III cities aligns well with government housing policies as well as continued urbanization trends in China."

Op basis van de kwartaalwinst van 94 cent per ADS en een koers van ca 2,58, komen we uit op een K/W van ca 0,70....!!!!

BeantwoordenVerwijderenhttp://finance.yahoo.com/news/xinyuan-real-estate-co-ltd-110000414.html

Die K/W van 0,7 is een beetje overdreven, omdat in de 94 cent een paar eenmalige posten zitten.

VerwijderenVoorlopig schat ik de winst voor dit jaar op ca 2,00 per ADS, de K/W zou dan uitkomen (bij een actuele koers van ca 3) op ca 1,5.

Xinyuan Real Estate: Still the World's Cheapest Stock

BeantwoordenVerwijderenTime:2012-07-05 Click: Author:Jared Sleeper print font:[bigmediumsmall]

A few months ago, I wrote an article asking if Xinyuan Real Estate (XIN), a property developer in China, was the world's cheapest stock. I pointed out the company's absurdly low valuationdescribed two potential reasons for it: fear of fraudfear of a Chinese housing market collapse. Since then, much has happened to Xinyuan,it now appears clear that fears about the Chinese housing market are not the primary reason Xinyuan remains undervalued (for those unfamiliar, the stock currently boasts a forward P/E of 2.34a P/B ratio of .33, compared to P/B ratios well above one for reasonably valued American homebuilders such as KB Home (KBH)Toll Brothers (TOL)).

The company beat its own estimates in the first quarter handily despite discounting some of its properties,with a third of the year gone reiterated its guidance for net income in the range of $97-$107 million for the full year, against a market cap of roughly $223 million. Instead, the market is clearly pricing significant, even imminent, fraud risk into XIN shares. In the original article, I listed many reasons why I thought fraud was particularly unlikely in Xinyuan's case, including its status as an IPO rather than a reverse mergermany similar frauds, its credible big-4 auditor (ErnstYoung),the company's history of returning value to shareholders through share buybacksdividends.

This generated massive doses of healthy skepticism in the comments section, making it clear that XIN has a way to go at convincing investors that its books are clean. However, despite valid points raised by some commenters, I remain of the persuasion that the odds of fraud in XIN's case are lower than the market seems to be pricing in, making this a potentially lucrative opportunity for investors to buy a quality company at a truly ridiculous discount to any reasonable valuation.

Before I set in to the reasons I believe Xinyuan is unlikely to be a fraud, I'dto explain why many investors might think it may be cooking its books. I can identify four primary reasons for this belief:

2)

BeantwoordenVerwijderen1. XIN's CFO, Tom Gurnee, was the chair of the audit committee at Longtop Financial Technologies, a company which ended up being a spectacular fraud, catching a prominent auditor (Deloitte) as well as many well-heeled hedge fund investors off guard. This case famously involved complicit Chinese banks who reported false cash balances to the auditors. Mr. Gurnee resigned his post at Longtopwas never charged in the incident, though it should rightly serve as a red flag for investors to take a closer look.

2. Xinyuan has a questionable transaction on record from April 2010, when the company raised $40 million using bonds at a very high interest rate (16%, 19% effective including attached warrants), despite what appeared to be a very strong liquidity position at the time. This was at the center of a laborious backforth with the SEC discussing various components of the company's filings.

3. Xinyuan is a Chinese small-cap stock. This alone, given the past year of spectacular collapses, is enough to raise significant skepticismeven drive some investors away. It remains possible that virtually all Chinese companies trading only in the U.S. have some form of accounting discrepancies,at least that accounting problems are very widespread.

4. Xinyuan remains very, very undervalued. For many, this alone raises the odds the company is fraudulent, as it seems logical that a reputable third party would have done its own due diligencepurchased the companya significant portions of its float given the stunning undervaluation,that the company's founder would have instigated a "going private" transactionmany wrongly undervalued Chinese small caps have. That this hasn't happenedthe stock remains undervalued is, inof itself, a red flag.

Standing on their own, these facts certainly lend credence to a degree of investor wariness about XIN's shares. When viewed holistically in context, however, the fraud case begins to look weaker.

http://en.xyre.com/content/details64_3812.html

Verwijderen3)

BeantwoordenVerwijderenStanding on their own, these facts certainly lend credence to a degree of investor wariness about XIN's shares. When viewed holistically in context, however, the fraud case begins to look weaker.

(1) Though details of the Longtop fraud remain murky, Mr. Gurnee did time as CFO of Sohu (SOHU), which is as reputable as companies in China get right now,is still chairman of the audit committee at eLong (LONG), a travel website in China that trades at a very healthy forward P/E of 20above its book value, strong signs that the market doesn't consider it a strong fraud contender. It is very possible that Mr. Gurnee was deceived at Longtop, especially given the depth of the fraud down to the bank level.

(2) Xinyuan's justification (see number 3) for its $40 million bond sale is that the company projected a financial shortfall for the year as it was planning massive land purchases (bank-borrowing to purchase land for development is illegal in China), but that the company ended up postponing said purchases due to the housing slowdown in China. In addition, the company was retiring $75million in bonds at the same time, so the result was still a substantial net outflow. Thus, the company has almost exclusively had negative cash flows from financing in recent years, making it look much less likely that the $40 million raise reflected a desperate need for additional capital to sustain operations despite an inflated balance sheet, as some likely suspect.

(3) Represents a classic case of guilt by association,is precisely why the potential profit is so large as time passes byinvestors learn of XIN's legitimacy.

(4) This remains a mystery to me. XIN's only major institutional holder, John Griffen's Blue Ridge Capital, continues to hold 20% of the float,XIN's founderchairman controls another 40%, leaving little room for other major holders without their buy-in dramatically moving the share price. Regardless, it seemsfactors (1), (2)(3) here are ruling the day, which the comments on my previous article seemed to prove.

Those aside, however, a series of events have occurred in the past few months that I believe make the case that XIN is legitimately much stronger than it was when the original article was published:

1. XIN announced a hefty quarterly dividend of $.04 per ADS (totaling .16 per year,more than 5%). This represents a substantial outlay of roughly $12 million dollars, which is very atypical behavior for a company that is overstating its financial position as said companies usually hoard cash to stay afloat.

2. Perhaps most importantly, XIN's 20-F (an SEC filing for foreign companies with shares in the U.S.) for the full year 2011 came back cleanly audited by ErnstYoung. Many will point out (rightly so) that this comes after a prominent failure by E&Y in the collapse of Sino-Forest, but it is important to note that this event occurred before the validation of Sino-Forest's latest yearly results,that it, paired with other prominent cases (including Longtop) likely made XIN's audit far more intensive than those in the past (for example, additional measures have been taken to avoid the bank complicity issue that arose during Longtop). In other words, though audit standards were clearly ineffective in the past, audits conducted after the recent blow-ups should carry higher weight as the auditors now have little room for error with their all-valuable reputations on the line,are being extra-careful.

3. XIN announced a surprise, $20 million share buyback program, representing a substantial percentage of its current float. Together with its dividend, the company will return $32 million to shareholders this year, 14% of the company's current market cap. It is key to note that this was unexpected; though the dividend had been pre-announced, XIN took this pro-shareholder step without any prior indication it would do so.

Albert Jones – Jones Capital Management

BeantwoordenVerwijderenWhat do large funds or any funds or any investors, what are their first questions to you as far as them taking that step to become a shareholder. What are their doubts? What are they asking you Tom and is it just a matter of the macro China thing right now and investors will eventually come back to legitimate companies. Well, I’m currently interested in the thoughts of the investors when you do road shows, what kind of questions do you get and what is stopping them from investing in your great company?

Tom Gurnee - Chief Financial Officer

Well, thanks for saying great company but first of all I would say the following. We are badly undervalued and those are too good to be true quality about us. And then I got to fight. I’ve got to get on the road and fight them.

Second is the fact that perhaps we use POC accounting and that’s maybe hard to understand but we’re required by U.S. GAAP to use it. The main concern of the large funds is liquidity that we have a small float and that they’re not going to be able to go in and out of large positions easily in our shares.

So it’s my job that I suggest I haven’t done it very well but it’s my job to try and get that liquidity up to these players. I need to get recognition from the investment community their numbers of real, they are repeatable, they are reliable and they are solid. And so in order to get some confidence in our shares. But U.S. what’s the main question I get. I get question about -- most often with larger funds is liquidity. It’s quite simple with that.

And then, there is concern about a bubble in China or there was. I don’t think people are talking about bubble anymore in China. They are talking about hard landing. I don’t think anybody is that convinced that China is going to be a real hard land. It may be a semi hard landing but nobody is talking about the bubble anymore right now in China.

And then there is the fraud risk. We have companies, Chinese companies that are -- there are too many frauds. In fact, I’ll say this publicly. I was audit committee chair of Longtop Financial and this company had fraud. And so it did happen anyway and that particular company, the CEO had worked on a scheme for up to years, three, four years before the IPO. And the IPO took place with Goldman and with Deutsche Bank with the auditors being devoid and we had extensive cash procedures there and we still had a fraud.

So this makes people little bit concerned. And I’m concerned, I mentioned earlier in my -- I'm concerned about what investors think. So we have in this company about 240 bank accounts. We reconciled every one of those matters every month and every one of those reconciliations is verified by H2. So there is two sets of buyers looking at that.

In addition, we recently implemented a cash verification procedure by internal audit and then finally we have an annual audit by EY that’s at the top of their game as far as increasing scrutiny over cash balances. So the best response I can give to investors like you is we’re doing our best to demonstrate the quality of our financial statements and the quality of our assets. Have I answered your question? I’m sorry, I talked in circle a little bit there.

http://seekingalpha.com/article/798291-xinyuan-s-ceo-discusses-q2-2012-results-earnings-call-transcript?page=6&p=qanda&l=last

BeantwoordenVerwijderen5 Stocks Trading Below Net Cash - Part II

August 19, 2012 | 12 comments | includes: GURE, LTON, MOBI, WKBT.PK, XNY

http://seekingalpha.com/article/815431-5-stocks-trading-below-net-cash-part-ii?source=yahoo

Shanda (GAME)- 2e kwartaal:

BeantwoordenVerwijderenNet Income Attributable to Ordinary Shareholders. Net income for the second quarter of 2012 was RMB308.4 million (US$48.8 million), an increase of 1.0% from RMB305.2 million in the second quarter of 2011 and a decrease of 8.4% from RMB336.8 million in the first quarter of 2012. Earnings per diluted ADS in the second quarter of 2012 were RMB1.10 (US$0.17), compared with RMB1.08 in the second quarter of 2011 and RMB1.20 in the first quarter of 2012.

Net Cash. In the second quarter of 2012 the Company generated RMB458.3 million (US$72.4 million) in cash flows from operating activities. The Company's cash and cash equivalent, short-term investments, restricted cash and time deposits, net of loans and dividend payable, increased from RMB2,664.9 million as of March 31, 2012 to RMB3,036.6 million (US$480.1 million) as of June 30, 2012.

First Half 2012 Unaudited Financial Results

Net Revenues. Net revenues for the first half of 2012 totaled RMB2,520.0 million (US$398.4 million), a decrease of 2.1% from RMB2,573.1 million in the first half of 2011.

Gross Profit. Gross profit for the first half of 2012 was RMB1,578.8 million (US$249.6 million), an increase of 1.1% from RMB1,561.9 million in the first half of 2011. Gross margin was 62.7%, an increase from 60.7% in the first half of 2011.

Operating Income. Operating income for the first half of 2012 was RMB790.8 million (US$125.0 million), an increase of 11.1% from RMB711.7 million in the first half of 2011. Operating margin was 31.4%, an increase from 27.7% in the first half of 2011.

Non-GAAP Operating Income. Non-GAAP operating income for the first half of 2012 was RMB883.8 million (US$139.7 million), an increase of 3.6% from RMB852.8 million in the first half of 2011. Non-GAAP operating margin was 35.1%, an increase from 33.1% in the first half of 2011.

Net Income Attributable to Ordinary Shareholders. Net income for the first half of 2012 was RMB645.2 million (US$102.0 million), an increase of 4.4% from RMB618.0 million in the first half of 2011. Net margin was 25.6%, an increase from 24.0% in the first half of 2011. Earnings per diluted ADS were RMB2.30 (US$0.36), compared with RMB2.18 in the first half of 2011.

Non-GAAP Net Income Attributable to Ordinary Shareholders. Non-GAAP net income for the first half of 2012 was RMB718.7 million (US$113.6 million), compared with RMB738.8 million in the first half 2011. Non-GAAP net margin was 28.5%, compared with 28.7% in the first half of 2011. Non-GAAP earnings per diluted ADS were RMB2.56 (US$0.40), compared with RMB2.60 in the first half of 2011.

Net Cash. In the first half of 2012 the Company generated RMB965.2 million (US$152.7 million) in cash flows from operating activities. The Company's cash and cash equivalent, short-term investments, restricted cash and time deposits, net of loans, increased from RMB2,160.1 million as of December 31, 2011 to RMB3,036.6 million (US$480.1 million) as of June 30, 2012.

Huidige koers ca 3,33.

VerwijderenK/W ca 4

ca 1,70 cash per aandeel.

Chinese gaming-aandelen doen het heel goed de laatste tijd, Shanda (GAME) staat op dit moment op ca 4,50.

VerwijderenFAB Universal: Overlooked By The Financial Community

BeantwoordenVerwijderenAug 13 2013, 08:25 | 4 comments | about: FU (Fab Universal Corp)

Disclosure: I have no positions in any stocks mentioned, but may initiate a long position in FU over the next 72 hours. My associate Anthony Orbanic assisted me with this article. (More...)

"FABulously Universal"- FAB Universal Looks to Become China's Leading Digital Media Distributor

FAB Universal Corp. (FU), a global distributor of digital entertainment content offered through such mediums as Netflix (NFLX)-like subscription models, standalone flagship locations, retail shops and standalone kiosks has had a very strong and busy 2013, especially in China. The company is the result of a brilliant transaction completed in the last quarter of 2012, whereby Wizard Software acquired FAB Universal Corp. and now the tail wags the dog.

FAB Universal generates revenues from these mediums and through continuing media content downloads, media membership cards, and kiosk based advertising. Customers can purchase and download copyrighted content directly to their mobile devices, giving Chinese consumers the one-two punch of a Netflix, Redbox or even an Amazon (AMZN).

According to a report from a leading audit firm, China's digital entertainment spending is over $90 billion (RMB 627 billion) a year. With a projected 11.6 percent compounding increase annually, spending is likely to reach $148 billion (RMB 959billion) by 2025.

FAB Universal's Key Distribution Partnerships

FAB Universal recently announced that it has increased its Intelligent Media kiosk business by 2,311 kiosks in the second quarter of this year, compared to 1,728 kiosks in the first quarter. This translates to an increase of 33.7% quarterly and 81% on a year-on-year basis.

The growth of the kiosk network alone has been tremendous over the last few years. Its network has grown to reach over 40 cities in China such as Beijing, Shenzhen, Chengdu and Guangzhou with some 16,000 kiosks installed. This resulted in the company selling 162,869 new membership cards in the second quarter, representing an increase in membership of 89% year over year .

On top of that, FAB Universal has also entered into agreements that will promote advertising revenue and further exposure and growth. FAB Universal signed a five year advertising agreement with Shanghai Qiujia Culture Media to provide advertising on menu screens of the FAB Intelligent Media Kiosk Network. The non-exclusive agreement is expected to yield $1.6 million for the company annually.

These developments are complemented by the company's expansion agreements with Time Antaeus Cinema and Shouhang Supermarkets to open multiple FAB branded media and entertainment retail locations. Based on their agreement, the partners will provide space for the company to operate their branded digital media stores and intelligent kiosks in key cities such as Beijing, Chengdu, and Guangzhou.

However this pales in comparison to the comparatively blockbuster deal that was signed with China Unicom (CHU) for FAB Universal to sell its products through authorized distributors Beijing Baifu Hongtai Technology Co., Ltd. (Beijing Baifu Hongtai) and Beijing Berlin Information Service co. Ltd. (Berlin Information Service).

Initially, Beijing Baifu Hongtai and Berlin Information Service will sell FAB Universal's copyright protected audio-video products in 37 China-Unicom Business Stores in Beijing.

2)

BeantwoordenVerwijderenStrong, Undervalued Fundamentals and Under-Reported Potential

FAB Universal 's growth and potential is also compounded by the presence of one of the legendary co-founders of the Quantum Fund, Jim Rogers. FAB Universal Chairman Zhang Hongcheng issued a statement saying that "We look forward to working with Mr. Rogers to represent the interests of FAB shareholders worldwide and help the company realize its tremendous potential. With Mr. Rogers' position and experience in the international financial community FAB has strengthened its leadership for our global expansion plans."

Currently no analyst coverage exists on FAB Universal. A curious uptick in average daily volume on August 13th, 2013 of 185,792 shares versus an average of 83,257 shares means that smaller investors can profit due to the lack of analyst coverage and institutional interest in FAB Universal as a lot of information. As these current developments have not been discounted into the stock price, any positive news is also buoyed by a staggering figure; sales have grown by an average of 40% a year over the past five years.

While the company was still in the red for the year ending Dec.31,2012, it has put out earnings guidance estimates of $0.60 for this year. Since the merger the most recent two quarters have been substantially in the black. At the current price of $4.44 at the time of this writing, this translates to FAB Universal trading at roughly six times earnings.

Currently digital media technology companies are trading at least 8 times earnings. For instance, communications solutions provider BCE Inc. (BCE) is trading at 13 times earnings and Apple Inc. (AAPL) is trading at 10 times earnings. If we assume that it would trade in line with its peers, FAB Universal would be valued at $6-$7 per share.

Given the current growth trends that range from intelligent media kiosks to streaming media, it would come as no surprise that the gap between price and value will close over the long run, especially as the Chinese digital media market continues to grow and more consumers in China start to see how "Fab" the digital world can be.

http://seekingalpha.com/article/1630992-fab-universal-overlooked-by-the-financial-community?source=yahoo

Verwijderen